Your insurance company has teams of adjusters, estimators, and claims specialists who handle thousands of roof damage cases every year. You, on the other hand, might file a roof claim once every 15 to 20 years. This imbalance creates a significant disadvantage for homeowners who assume the first settlement offer reflects what their policy actually covers.

The stakes are substantial. A typical roof replacement in Texas costs between $8,000 and $25,000 for most single-family homes, with the average falling around $12,000 to $17,000 depending on materials and roof size. When an initial insurance estimate comes in thousands of dollars below what the work actually costs, many homeowners either pay the difference out of pocket or accept inadequate repairs that fail prematurely.

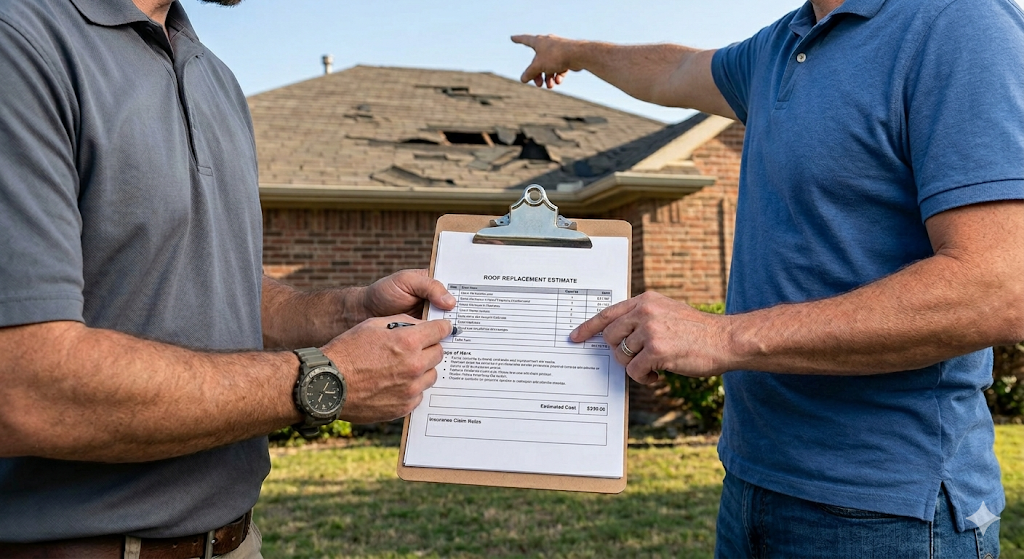

Here is what most homeowners do not realize: the initial settlement offer is rarely final. You have the right to challenge the scope, pricing, and completeness of your insurance company’s estimate. This is not about haggling or asking for favors. It is about ensuring your insurer pays what your policy entitles you to receive. This guide explains exactly how to negotiate a fair roof replacement settlement in Texas, from building your case to escalating disputes when necessary.

Understanding What You Can and Cannot Negotiate

Before you begin any negotiation, understand what is actually on the table. Many homeowners believe they can negotiate their deductible, but Texas law explicitly prohibits this. Under House Bill 2102, contractors cannot waive, rebate, or absorb a homeowner’s deductible, and any arrangement to do so is illegal. If a contractor offers to cover your deductible, walk away immediately, as this is a red flag for potential fraud that could jeopardize your entire claim.

What you can negotiate includes the scope of damage the insurer acknowledges, the materials and labor pricing used in their estimate, coverage for code upgrades required by current building standards, and any line items the adjuster missed during inspection. The negotiation centers on proving that your claim is worth more than the initial offer based on documented evidence, not on personal appeals or complaints.

Your policy type significantly affects the negotiation. Replacement Cost Value policies pay the full cost to replace your roof with similar materials, while Actual Cash Value policies deduct depreciation based on your roof’s age. With RCV coverage, you typically receive an initial payment reflecting the depreciated value, then a second payment for the recoverable depreciation after you complete repairs and submit proof. Understanding this two-payment structure is essential for knowing what you should ultimately receive.

Why Insurance Estimates Are Often Too Low

Insurance adjusters work for the insurance company, not for you. Their job is to assess damage accurately, but their incentives do not always align with paying the maximum amount your policy allows. Initial estimates frequently fall short of actual replacement costs for several predictable reasons.

Adjusters often miss damage that is not immediately visible. Bruised shingles that will fail prematurely, compromised underlayment, damaged flashing around penetrations, and soft spots in the decking may not be obvious from a quick inspection. During peak storm season, when adjusters are handling dozens of claims per week, inspections tend to be faster and less thorough.

Pricing discrepancies are another common issue. Insurance companies use estimating software with pricing databases that may not reflect current material costs or local labor rates. Roofing materials have seen significant price increases in recent years, and estimates based on outdated figures leave homeowners with a gap between the settlement and actual costs. Additionally, adjusters sometimes fail to account for code upgrades that are now required but were not part of the original roof installation, such as enhanced deck attachment or specific underlayment requirements.

The key point is that the initial estimate represents a starting position, not a final determination. Insurance companies expect some claims to be supplemented, and the process exists precisely because first estimates are often incomplete.

Build Your Case Before You Negotiate

Successful negotiation requires evidence. Before you challenge your insurance company’s estimate, you need documentation that supports a higher valuation. This preparation separates homeowners who receive fair settlements from those who accept whatever is initially offered.

Get an Independent Professional Roof Inspection

Schedule a professional roof inspection with a qualified roofing contractor in Allen or your local area before or immediately after the adjuster visits. A thorough contractor inspection often identifies damage the adjuster misses: areas where shingle roofing shows bruising that will lead to premature failure, compromised underlayment beneath shingles that appear intact, flashing damage around vents and chimneys, and decking that has taken impact damage.

Request a detailed written estimate that breaks down every component: tear-off and disposal, materials with specific product names and quantities, labor, permits, code compliance items, and any specialty work required. This line-item format allows you to compare directly against the adjuster’s estimate and identify specific discrepancies.

Document Everything in Writing

Photograph and video all damage from multiple angles, including both exterior roof damage and any interior evidence such as water stains or wet insulation. Save weather data from the National Weather Service that links the damage to a specific covered event. Keep all correspondence with your insurance company in written form, whether email or certified mail. Request a copy of the adjuster’s full report and line-item estimate, not just the summary.

Compare Estimates Line by Line

With both estimates in hand, compare them systematically. Look for line items that appear in your contractor’s estimate but are missing from the adjuster’s. Check pricing per square for materials and labor. Note any code upgrade requirements your contractor includes that the adjuster omitted, such as enhanced deck attachment, ice and water shield in valleys, or specific underlayment types now required by Texas building codes. Each discrepancy becomes a specific point you can address in your supplement request.

The Supplement Process Explained

A supplement is a formal request for additional payment when the initial insurance estimate does not cover the full cost of necessary repairs or replacement. This is the primary mechanism for negotiating a fair roof replacement settlement, and it is a normal part of the claims process that insurance companies handle regularly.

File a supplement when your contractor’s estimate exceeds the adjuster’s estimate, when hidden damage is discovered during the repair process, or when code upgrades are required that were not included in the original scope. The supplement should include your contractor’s detailed estimate, photographs documenting the additional damage or work needed, and a written explanation of why each additional item is necessary and covered under your policy.

Texas Insurance Code Section 2706 requires insurers to respond to supplement requests within 30 days. If your supplement is approved, you receive additional payment. If denied, you have the right to escalate through other channels. Many supplements are partially approved, with some items accepted and others rejected, which may lead to further negotiation or escalation.

Be prepared for the supplement process to take time. Complex claims may require multiple rounds of documentation and communication. Patience and persistence, backed by solid documentation, typically yield better results than accepting an inadequate initial offer.

Working with Your Contractor During Negotiation

Texas law places important restrictions on what contractors can do in the claims process. Under Texas Insurance Code Section 4102.163, contractors cannot act as public insurance adjusters or advertise that they will negotiate claim settlements on your behalf. Any contractor who promises to “handle everything with your insurance company” or “get you every dollar you deserve” is likely violating state law.

However, contractors can provide substantial legitimate support. They can give you detailed estimates that serve as the foundation for your supplement request. They can document damage with professional photographs and written reports. They can meet with the adjuster during the inspection to ensure all damage is observed and noted. They can discuss scope and pricing clarifications with the insurance company regarding their own estimate. A GAF Master Elite certified contractor brings credibility and expertise that strengthens your position.

Having your contractor present during the adjuster’s inspection is particularly valuable. An experienced contractor knows where to look for damage that adjusters sometimes miss and can point out issues in real time. This often results in a more complete initial estimate, reducing the need for extensive supplementation later.

The Appraisal Clause Option

If supplement negotiations reach an impasse, most Texas homeowner policies include an appraisal clause that provides a binding resolution mechanism for valuation disputes. This is not the same as an appeal or a lawsuit. Appraisal is specifically designed to resolve disagreements about how much the loss is worth when coverage itself is not in question.

The appraisal process works as follows: you hire an appraiser and your insurance company hires an appraiser. The two appraisers then select a neutral umpire. Each appraiser submits an independent assessment of the loss. If the two appraisers agree, that becomes the binding determination. If they disagree, the umpire makes the final decision, and any two of the three agreeing sets the binding award.

You pay for your own appraiser and half of the umpire’s fees. Typical costs for homeowners range from $1,000 to $5,000 depending on the complexity of the claim. Because of these costs, appraisal generally makes sense only when the gap between your estimate and the insurer’s offer is substantial, typically $5,000 or more.

One critical limitation: appraisal determines the amount of loss only, not coverage disputes. If your insurer is denying coverage entirely or claiming the damage is excluded, appraisal is not the appropriate remedy. It is designed for situations where both sides agree the damage is covered but disagree on how much the repair should cost.

Other Escalation Options

Beyond supplements and appraisal, several other escalation paths exist for homeowners who believe they are not receiving a fair settlement.

Request a re-inspection with a different adjuster. Sometimes the original adjuster missed damage or made errors, and a second set of eyes catches what the first inspection overlooked. This is a reasonable request that insurance companies routinely accommodate.

Consider hiring a public adjuster. Licensed by the Texas Department of Insurance, public adjusters work on behalf of homeowners to negotiate claim settlements. They charge fees for their services, capped at 10 percent of the claim amount under Texas law. For complex claims or significant disputes, their expertise may justify the cost, particularly if they can secure a substantially higher settlement.

File a complaint with the Texas Department of Insurance if you believe your insurer is acting in bad faith or violating state regulations. While TDI cannot force payment, documented complaints create pressure and establish a record of the insurer’s conduct. The consumer helpline is 800-252-3439.

Consult with an insurance dispute attorney for significant claims where other methods have failed. Many Texas attorneys who handle insurance disputes work on contingency, meaning you pay nothing unless you win. Under Texas law, if you prevail in an insurance dispute lawsuit, the insurer must pay your attorney fees, which removes much of the financial risk from pursuing legal action.

Key Texas Laws Protecting Homeowners

Understanding your legal rights strengthens your negotiating position. Texas has several laws specifically designed to protect homeowners in insurance disputes.

Texas Insurance Code Section 2707 requires insurers to acknowledge your claim within 15 days of receiving notice and to provide you with the name of the adjuster handling your claim along with information about your policy rights.

Texas Insurance Code Section 2706 requires insurers to accept or deny your claim within 30 days after receiving all documentation and items requested. This same 30-day timeline applies to supplement requests. If the insurer needs more time due to matters beyond their control, they must notify you in writing.

Texas Insurance Code Section 542.060 imposes penalty interest on insurers who fail to comply with prompt payment requirements. If your insurer delays payment beyond the statutory deadlines without justification, you may be entitled to interest on the unpaid amount.

You have one year from the date of loss to file a claim under most Texas policies. Missing this deadline can result in a complete denial, regardless of how valid your claim might be.

Finally, Texas law protects your right to choose your own contractor. Your insurance company cannot require you to use their preferred vendor network or a specific contractor. You select who performs roof repairs or replacement on your home.

Common Mistakes That Weaken Your Position

Many homeowners undermine their own negotiating position through avoidable errors. Accepting the first offer without review is the most common mistake. The initial estimate is a starting point, and reviewing it carefully against an independent contractor assessment is essential.

Failing to get an independent contractor estimate leaves you without the documentation needed to challenge an inadequate offer. Without a detailed competing estimate, you have no specific basis for requesting additional payment.

Making permanent repairs before the adjuster sees the damage can jeopardize your claim. Emergency tarping and water mitigation are appropriate, but completing a full roof replacement before the insurance company documents the damage may result in denied or underpaid claims.

Poor documentation weakens every aspect of your claim. Without thorough photos, written records, and preserved evidence, you cannot prove the extent of damage or support your requested settlement amount.

Working with storm chasers who appear after major weather events creates multiple problems. These contractors often have no local presence, limited accountability, and may disappear before warranty issues arise. Choose a reputable local contractor with an established track record, proper licensing, and manufacturer certifications like roofing contractor in Plano or other DFW communities where they have completed work and can provide references.

Get Expert Support for Your Roof Claim Today!

If you have received a roof damage estimate from your insurance company and believe it falls short of what your repairs will actually cost, contact Pickle Roofing Solutions for a free inspection and detailed estimate. We document all damage thoroughly, provide line-item estimates that can support supplement requests, and can meet with your adjuster to ensure nothing is overlooked. Our goal is to help you receive a fair settlement so your roof can be properly restored. Call (469) 247-8310 or visit our contact page to schedule your inspection today.

Frequently Asked Questions

Can I negotiate my insurance deductible?

No. Texas law under House Bill 2102 prohibits contractors from waiving, rebating, or absorbing your deductible. Any contractor who offers to do so is breaking the law, and participating in such an arrangement can jeopardize your claim and expose both you and the contractor to legal penalties including fines up to $2,000 and up to 180 days in jail.

What is a supplement and when should I file one?

A supplement is a formal request for additional payment when your contractor’s estimate exceeds the adjuster’s initial offer. File a supplement when line items are missing from the insurance estimate, when pricing falls below current market rates, when hidden damage is discovered during repairs, or when code upgrades are required that were not included in the original scope.

How long does the insurance company have to respond to my claim?

Under Texas Insurance Code Section 2707, insurers must acknowledge your claim within 15 days of receiving notice. Under Section 2706, they must accept or deny the claim within 30 days after receiving all requested documentation. The same 30-day timeline applies to supplement requests.

What is the difference between RCV and ACV coverage?

Replacement Cost Value coverage pays the full cost to replace your roof with similar materials without deducting for depreciation. Actual Cash Value coverage deducts depreciation based on your roof’s age and condition, often resulting in significantly lower payouts. With RCV coverage, you typically receive the depreciated amount initially, then the recoverable depreciation after completing repairs and submitting documentation.

Should I hire a public adjuster?

Consider hiring a public adjuster for complex claims, significant disputes, or if you feel overwhelmed by the process. Public adjusters are licensed by the Texas Department of Insurance and charge fees capped at 10 percent of the claim amount. Weigh the cost against the potential increase in settlement. For simple claims with modest disputes, the expense may not be justified.

What happens if my claim is denied after I appeal?

If your claim remains denied after appeals, you can invoke the appraisal clause to resolve valuation disputes, file a complaint with the Texas Department of Insurance at 800-252-3439, or consult with an insurance attorney. Many attorneys work on contingency, and under Texas law, the insurer must pay your attorney fees if you prevail in court.

About Pickle Roofing Solutions

Pickle Roofing Solutions is a GAF Master Elite certified roofing contractor serving Allen, Plano, Frisco, McKinney, and communities throughout the Dallas-Fort Worth metroplex. Our team provides detailed damage documentation, professional estimates, and support through the insurance claims process, including meeting with adjusters to ensure all damage is properly identified. We back our work with manufacturer warranty options and remain in the community long after the job is complete.